Existing home sales inch up in July on modest pullback in mortgage rates

Sales of previously occupied U.S. homes rose in July as homebuyers were encouraged by a modest pullback in mortgage rates, slowing home price growth and the most properties on the market in over five years.Recommended VideoExisting home sales rose 2% last month from June to a seasonally adjusted annual rate of 4.01 million units, the National Association of Realtors said Thursday.Sales edged up 0.8% compared with July last year. The latest sales figure topped the 3.92 million pace economists were expecting, according to FactSet.Home prices rose on an annual basis for the 25th consecutive month, although the rate of growth continued to slow. The national median sales price inched up just 0.2% in July from a year earlier to $422,400.That was the smallest annual increase since June 2023. Even so, the median home sales price last month is the highest for any previous July, based on data going back to 1999.“The ever-so-slight improvement in housing affordability is inching up home sales,” said Lawrence Yun, NAR’s chief economist. “Wage growth is now comfortably outpacing home price growth, and buyers have more choices.”The U.S. housing market has been in a sales slump since 2022, when mortgage rates began climbing from historic lows. Sales of previously occupied U.S. homes sank last year to their lowest level in nearly 30 years.This year’s spring homebuying season, which is traditionally the busiest period of the year for the housing market, was a bust as stubbornly high mortgage rates put off many prospective homebuyers. Affordability remains a dauting challenge for most aspiring homeowners following years of skyrocketing home prices.First-time homebuyers, who don’t have home equity gains to put toward a new home purchase, accounted for 28% of homes sales last month, down from 30% in June, NAR said. Historically, they made up 40% of home sales.The average rate on a 30-year mortgage has remained elevated this year, although it has been at a nearly 10-month low of 6.58% the last two weeks.Homes purchased last month likely went under contract in May and June, when the average rate ranged from 6.76% to 6.89%. Mortgage rates eased in July, dropping briefly to 6.67%.As home sales have slowed, the number of unsold homes on the market has been rising.There were 1.55 million unsold homes at the end of last month, up 0.6% from June and 15.7% from July last year, NAR said. That’s the most homes on the market since May 2020, early on in the COVID-19 pandemic.Still, the inventory remains well below the roughly 2 million homes for sale that was typical before the pandemic.July’s month-end inventory translates to a 4.6-month supply at the current sales pace, down from a 4.7-month supply at the end of June and up from 4 months in July last year. Traditionally, a 5- to 6-month supply is considered a balanced market between buyers and sellers.Homes are also taking longer to sell. Properties typically remained on the market for 28 days last month before selling, up from 24 days in July last year, NAR said.Home shoppers who can afford to buy at current mortgage rates or pay in cash are likely to benefit from the slower growth in prices and increased supply of properties on the market.It’s not uncommon now for sellers, especially those in Southern and Western markets, to lower their asking price and offer incentives such as money for closing costs or repairs in order to sweeten the deal, real estate agents say.In July, some 20.6% of homes listed for sale had their price reduced, according to Realtor.com. That’s down slightly from June.“One can say that things are a little better today as a buyer, compared to say just a couple of years ago,” Yun said.Join us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

‘Just another nail in the coffin for rural areas’: Affordable housing program faces the axe under Trump’s tax, budget cuts

Heather Colley and her two children moved four times over five years as they fled high rents in eastern Tennessee, which, like much of rural America, hasn’t been spared from soaring housing costs.Recommended VideoA family gift in 2021 of a small plot of land offered a shot at homeownership, but building a house was beyond reach for the 45-year-old single mother and manicurist making $18.50 an hour.That changed when she qualified for $272,000 from a nonprofit to build a three-bedroom home because of a grant program that has helped make affordable housing possible in rural areas for decades. She moved in last June.“Every time I pull into my garage, I pinch myself,” Colley said.Now, President Donald Trump wants to eliminate that grant, the HOME Investment Partnerships Program, and House Republicans overseeing federal budget negotiations did not include funding for it in their budget proposal. Experts and state housing agencies say that would set back tens of thousands of future affordable housing developments nationwide, particularly hurting Appalachian towns and rural counties where government aid is sparse and investors are few.The program has helped build or repair more than 1.3 million affordable homes in the last three decades, of which at least 540,000 were in congressional districts that are rural or significantly rural, according to an Associated Press analysis of federal data.“Maybe they don’t realize how far-reaching these programs are,” said Colley, who voted for Trump in 2024. Among those half a million homes that HOME helped build, 84% were in districts that voted for him last year, the AP analysis found.“I understand we don’t want excessive spending and wasting taxpayer dollars,” Colley said, “but these proposed budget cuts across the board make me rethink the next time I go to the polls.”The HOME program, started under President George H. W. Bush in the 1990s, survived years of budget battles but has been stretched thin by years of rising construction costs and stagnant funding. That’s meant fewer units, including in some rural areas where home prices have grown faster than in cities.The program has spent more than $38 billion nationwide since it began filling in funding gaps and attracting more investment to acquire, build and repair affordable homes, HUD data shows. Additional funding has gone toward projects that have yet to be finished and rental assistance.HOME’s future is in political limboTo account for the gap left by the proposed cuts, House Republicans want to draw on nearly $5 billion from a related pandemic-era fund that gave states until 2030 to spend on projects supporting people who are unhoused or facing homelessness.That $5 billion, however, may be far less, since many projects haven’t yet been logged into the U.S. Department of Housing and Urban Development’s tracking system, according to state housing agencies and associations representing them.A spokesperson for HUD, which administers the program, said HOME isn’t as effective as other programs where the money would be better spent.In opposition to Trump, Senate Republicans have still included funding for HOME in their draft budget. In the coming negotiations, both chambers may compromise and reduce but not terminate HOME’s funding, or extend last years’ overall budget.White House spokesperson Davis Ingle didn’t respond to specific questions from the AP. Instead, Ingle said that Trump’s commitment to cutting red tape is making housing more affordable.A bipartisan group of House lawmakers is working to reduce HOME’s notorious red tape that even proponents say slows construction.Some rural areas are more dependent on HOMEIn Owsley County — one of the nation’s poorest, located in the rural Kentucky hills — residents struggle in an economy blighted by coal mine closures and declining tobacco crop revenues.Affordable homes are needed there, but tough to build in a region that doesn’t attract larger-scale rental developments that federal dollars typically go toward.That’s where HOME comes in, said Cassie Hudson, who runs Partnership Housing in Owsley, which has relied on the program to build the majority of its affordable homes for at least a dozen years.A lack of additional funding for HOME has already made it hard to keep up with construction costs, Hudson said, and the organization builds a quarter of the single-family homes it used to.“Particularly for deeply rural places and persistent poverty counties, local housing developers are the only way homes and new rental housing gets built,” said Joshua Stewart of Fahe, a coalition of Appalachian nonprofits.That’s in part because investment is scant and HOME steps in when construction costs exceed what a home can be sold for — a common barrier in poor areas of Appalachia. Some developers use the profits to build more affordable units. Its loss would erode those nonprofits’ ability to build affordable homes in years to come, Stewart said.One of those nonprofits, Housing Development Alliance, helped Tiffany Mullins in Hazard, Kentucky, which was ravaged by floods. Mullins, a single mother of four who makes $14.30 an hour at Walmart, bought a house there thanks to HOME funding and moved in August.Mullins sees the program as preserving a rural way of life, recalling when folks owned homes and land “with gardens, we had chickens, cows. Now you don’t see much of that.”It’s a long-term impactIn congressional budget negotiations, HOME is an easier target than programs such as vouchers because most people would not immediately lose their housing, said Tess Hembree, executive director of the Council of State Community Development Agencies.The effect of any reduction would instead be felt in a fizzling of new affordable housing supply. When HOME funding was temporarily reduced to $900 million in 2015, “10 to 15 years later, we’re seeing the ramifications,” Hembree said.That includes affordable units built in cities. The biggest program that funds affordable rental housing nationwide, the Low Income Housing Tax Credit, uses HOME grants for 12% of units, totaling 324,000 current individual units, according to soon-to-be-published Urban Institute research.Trump’s spending bill that Republicans passed this summer increased LITHC, but experts say further reducing or cutting HOME would make those credits less usable.“It’s LITHC plus HOME, usually,” said Tim Thrasher, CEO of Community Action Partnership of North Alabama, which builds affordable apartments for some of the nation’s poorest.In the lush mountains of eastern West Virginia, Woodlands Development Group relies on HOME for its smaller rural projects. Because it helps people with a wider range of incomes, HOME is “one of the only programs available to us that allows us to develop true workforce housing,” said executive director Dave Clark.It’s those workers — nurses, first responders, teachers — that nonprofits like east Tennessee’s Creative Compassion use HOME to build for. With the program in jeopardy, grant administrator Sarah Halcott said she fears for her clients battling rising housing costs.“This is just another nail in the coffin for rural areas,” Halcott said.___Kramon reported from Atlanta. Bedayn reported from Denver. Herbst contributed from New York City, and Kessler reported from Washington, D.C.___Kramon is a corps member for The Associated Press/Report for America Statehouse News Initiative. Report for America is a nonprofit national service program that places journalists in local newsrooms to report on undercovered issues.Join us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

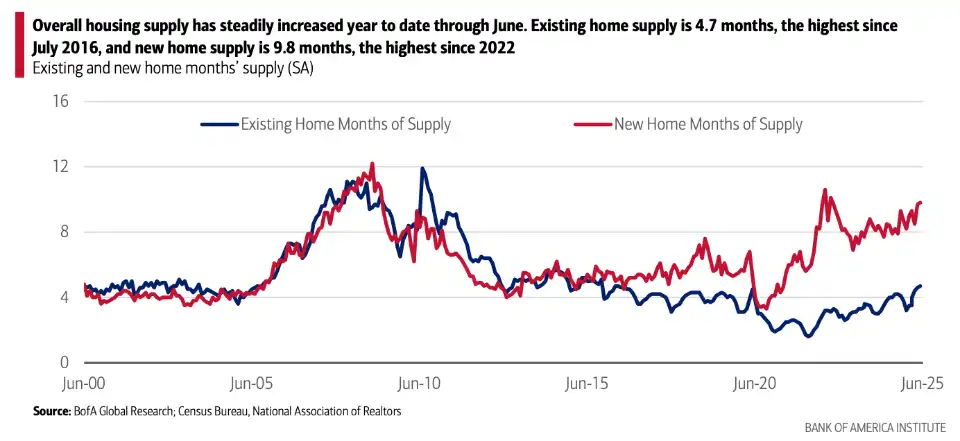

New home inventory is at its highest level since just before the housing market collapse that led to the Great Recession, but that doesn’t mean it’s the same market

The U.S. housing market’s inventory is growing, putting pressure on prices and slowing new construction, according to fresh research from the Bank of America Institute. As of June, existing-home supply reached 4.7 months, the highest level since July 2016. New-home supply surged even further to 9.8 months—its highest point since 2022—highlighting how quickly inventory is building across the housing market.Recommended VideoThe influx of available homes reflects sluggish demand, with builders citing weak buyer urgency, affordability challenges, and lingering job instability. The Institute noted new-home inventory is now at its highest level since 2007, the year before the housing market collapse that led to the Great Financial Crisis.ResiClub co-founder Lance Lambert toldFortunethat the rising inventory tells us that “homebuyers are gaining leverage” as slack in the housing market is increasing. “The Pandemic Housing Boom saw too much housing demand all at once, home prices overheated too fast in many markets, and underlying fundamentals got too stretched.”Lambert characterized the last few years as a “recalibration period” where the housing market is smoothing out that excess. Mounting inventory sucks out appreciation in more markets—and even causes outright corrections in some markets’ home prices. He said he expects the underlying fundamentals to slowly improve as that happens and incomes keep rising. “It takes time.” This period is different from 2007, he said, because that window saw a far greater weakening of the housing market and upswing in resale inventory, along with unsold, completed newbuild homes.BofA ResearchOne striking shift: The median price of a new home has actually fallen below that of an existing home—a reversal of the usual market dynamic. BofA said this pricing inversion underscores how builders are being forced to discount amid rising supply and softer demand. “Builders are starting to pull back on new home starts in many markets,” Bank of America wrote. While the slowdown is broad-based, conditions vary regionally, with some areas such as the Midwest proving more resilient than others.“Since the Pandemic Housing Boom fizzled out in 2022, and the affordability squeeze was fully felt,” Lambert toldFortune, “the national power dynamic has slowly been shifting from sellers to buyers as homes have a harder time selling and active inventory for sale builds.”Still, Lambert noted the inventory picture varies significantly across the country. For instance, it remains most limited across notable sections of the Midwest and the Northeast, although still growing, he said. On the other hand, active inventory has neared or surpassed pre-pandemic 2019 levels in many parts of the Sun Belt and Mountain West, and he said that is where homebuyers have gained the most leverage.The trend comes as the Federal Reserve has begun trimming interest rates in an effort to support both broader economic growth and housing affordability. Whether those cuts will be enough to reignite demand remains an open question.For now, the data signals a market in transition: high inventory, moderating prices, and builders caught between a cautious consumer and the need to manage supply.For this story, Fortune used generative AI to help with an initial draft. An editor verified the accuracy of the information before publishing. Join us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

30-year mortgage rate holds steady at lowest level in nearly 10 months

The average rate on a 30-year U.S. mortgage held steady this week at its lowest level in nearly 10 months, an encouraging sign for prospective homebuyers who have been held back by stubbornly high home financing costs.Recommended VideoThe long-term rate was unchanged from last week at 6.58%, mortgage buyer Freddie Mac said Thursday. A year ago, the rate averaged 6.46%.Borrowing costs on 15-year fixed-rate mortgages, popular with homeowners refinancing their home loans, edged lower. The average rate dropped to 5.69% from 5.71% last week. A year ago, it was 5.62%, Freddie Mac said.Stubbornly high mortgage rates have helped keep the U.S. housing market in a sales slump since early 2022, when rates started to climb from the rock-bottom lows they reached during the pandemic. Home sales sank last year to their lowest level in nearly 30 years and have remained sluggish this year.For much of the year, the average rate on a 30-year mortgage has hovered relatively close to its 2025 high of just above 7%, set in mid-January. Since last week, the average rate has been at its lowest level since Oct. 24, when it averaged 6.54%.Mortgage rates are influenced by several factors, from the Federal Reserve’s interest rate policy decisions to bond market investors’ expectations for the economy and inflation.The main barometer is the 10-year Treasury yield, which lenders use as a guide to pricing home loans. The yield was at 4.34% at midday Thursday, up from 4.29% late Wednesday.The yield has been mostly rising this month as bond traders weighed how data on inflation and the job market, and the potential economic impact of Trump administration’s tariffs, may influence the Fed’s interest rate policy moves.The central bank has so far been hesitant to cut interest rates out of fear that Trump’s tariffs could push inflation higher, but data showing hiring slowed last month have fueled speculation that the Fed will cut its main short-term interest rate next month.A Fed rate cut could give the job market and overall economy a boost, but it could also fuel inflation, which could push bond yields higher, driving mortgage rates upward in turn.“Even if the Fed cuts the short-term federal funds rate in September, which is largely expected, it is not likely that we will see a big drop in mortgage rates,” said Lisa Sturtevant, chief economist at Bright MLS.Economists generally expect the average rate on a 30-year mortgage to remain near the mid-6% range this year.That may not be low enough to spur a meaningful increase in home sales.While the housing market slowdown is forcing many sellers to lower their asking price and even pay for a buyer’s closing costs, among other incentives, affordability remains a major hurdle for many aspiring homeowners.Home price growth has slowed nationally, but the median sales price of a previously occupied U.S. home remains near the all-time high of $435,300 set in June. And while prices are down from a year ago in many metro areas in the South and West such as Miami, Denver and Austin, they haven’t come down nearly enough to offset years of soaring prices.“Lower mortgage rates and slower price growth — or even year-over-year price declines — is going to be necessary to improve affordability and bring more homebuyers into the market,” Sturtevant said.Join us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

More than half of U.S. homes have dropped in value over the last year—and nearly all houses in these cities have seen losses

The share of U.S. homes that have lost value in the past year is the highest since the aftermath of the Great Recession, according to Zillow.Recommended VideoIn October, 53% of homes saw their “Zestimates” decline, the most since 2012 and up from just 16% a year earlier. Losses were most widespread in the West and South.In fact, those regions have housing markets where nearly all homes declined in value over the last year. Denver topped the list with 91%, followed by Austin (89%), Sacramento (88%), Phoenix (87%), and Dallas (87%).The Northeast and Midwest, by contrast, have largely avoided such losses, but declines are spreading to more homes in all metros, Zillow said.In addition, most homes also dropped from their peak valuations, with the average drawdown hitting 9.7%. While that has soared from 3.5% in the spring of 2022, it’s still well below the 27% average drawdown in early 2012.To be sure, lower home values are just losses on paper and aren’t realized by homeowners unless actual sale prices undercut their initial purchase prices.By that score, homeowners are still ahead as Zillow data shows that values are up a median 67% since the last sale, and just 4.1% of homes have lost value since their last sale.“Homeowners may feel rattled when they see their Zestimate drop, and it’s more common in today’s cooler market environment than in recent years. But relatively few are selling at a loss,” Treh Manhertz, senior economic researcher at Zillow, said in a statement. “Home values surged over the past six years, and the vast majority of homeowners still have significant equity. What we’re seeing now is a normalization, not a crash.”ZillowThe lower values come as the housing market has been frozen for much of the past three years after rate hikes from the Federal Reserve in 2022 and 2023 sent borrowing costs higher, discouraging homeowners from giving up their existing ultralow mortgage rates.But the dearth of new supply kept home prices high, shutting out many would-be homebuyers who were also balking at elevated mortgage rates.With demand weak, the housing market has been shifting away from sellers and toward buyers. The pendulum has swung so far the other way that delistings soared this year as sellers became fed up with offers coming in below asking prices and just take their homes off the market.But the National Association of Realtors sees a turnaround coming next year. NAR chief economist Lawrence Yun predicted earlier this month existing-home sales will jump 14% in 2026 after three years of stagnation, with new-home sales rising 5%. Those sales will support a 4% uptick in home prices.“Next year is really the year that we will see a measurable increase in sales,” Yun said at a conference on Nov. 14. “Home prices nationwide are in no danger of declining.”

The mortgage rate decline it would take to make an average home affordable is ‘unrealistic,’ Zillow says

Since the pandemic, U.S. mortgage rateshave risen dramatically. This surge, combined with historically high home prices, has tanked housing affordability, with first-time homebuyer rates falling to half the historical average. Even a substantial drop in mortgage rates would not restore housing affordability for most Americans.During the pandemic, one of the few things people enjoyed were low mortgage rates. From spring 2020 through 2021, mortgage rates were around or even below 3%. Rates steadily crept up during 2022 and 2023, peaking at 8% in late 2023.Recommended VideoAt the time, economists warned home buyers to get used to high mortgage rates. Today, mortgage rates are still nearly 7%. High mortgage rates have been just one facet of the housing affordability crisis in the U.S. Home prices are also historically high—up more than 53% since the onset of the pandemic. As a result, the number of first-time homebuyers is half the historical norm. In order for a typical home to be affordable to a buyer, mortgage rates would need to drop to 4.43%, Zillow economic analyst Anushna Prakash reported Tuesday. But “that kind of a rate decline is currently unrealistic,” she said. Meanwhile, not even a 0% interest rate would make a typical home affordable in New York, Los Angeles, Miami, San Francisco, San Diego, or San Jose, according to Zillow.“It’s unlikely rates will drop to the mid-[4% range] anytime soon,” Arlington, Va.-based real estate agent Philippa Main toldFortune. “And even if they did, housing prices are still at historic highs.” With 11 years of experience, Main is also a licensed mortgage loan officer The factors affecting housing affordability in the U.S.Prakash’s analysis holds income, home prices, and all other housing-related costs equal. This gets at the crux of the ongoing issues of the U.S. housing market: There are a variety of factors that affect housing affordability. And even if one were to change drastically, it wouldn’t result in a sudden affordability surge for hopeful home buyers. “While lower rates certainly help, they are just one piece of a far more complex puzzle that includes inventory shortages, wage stagnation, and rising insurance and tax costs,” James Schenck, CEO of PenFed Credit Union, toldFortune. “In other words, housing affordability is about more than just the Fed—it’s about the full ecosystem of access and equity.”Wages haven’t kept up with home prices: Rents and house prices have been rising faster than incomes across most regions of the U.S., according to a 2024 report from the U.S. Department of the Treasury. In turn, Americans need to make more than six figures to afford a median-priced home, according to Realtor.com, but the average salary in the U.S. is only slightly more than half of that. “Even in markets that have seen a heavy correction and have lost 10% [or more] of value, homes are still selling for a higher percentage of people’s average income, making them feel more expensive than they did five years ago,” Main explained. She encourages her clients to look for a home that meets 85% to 90% of their criteria—say living further away or having one less bedroom—to have a shot at actually finding a home that’s affordable for them. That can be frustrating, though, considering that housing is so expensive “people don’t want to compromise because they feel they are committing so much more financially.”Combating deteriorating housing affordabilityEven if you can’t buy your dream home initially, there are other options to make it feel that way after it’s been yours for a while. More people are pouring home equity into renovations and staying in place instead of shelling out for a more expensive home at the start. Plus, being more modest from the outset can put you on a better path for eventually buying a new home.“It’s easier to buy your dream home once you’ve built equity in another home you can sell, than it is to hold out for the perfect fit while still renting,” Main said, who also suggested looking at homes that have been on the market for longer. Sellers might be more willing to negotiate prices or give closing cost credits or mortgage rate buy downs, she added. There are also various mortgage options through smaller banks and credit unions, as well as special VA rates and adjustable-rate mortgages (ARM) that can be more affordable for some borrowers. Because credit unions are structured differently from for-profit mortgage lenders, they can offer lower loan rates and fees, Schenck explained.“We aren’t waiting for the market to change,” he said. Main also said mortgage rates from local banks and credit unions can be more lucrative for some home buyers, but it’s important to know what’s the best fit financially for a home buyer. One of her clients recently got a lower interest rate through a local credit union, but it’s an ARM that will ultimately change to an unknown rate in the future. “It got them in the home they wanted at the monthly payment they can afford, and they plan to refinance into a traditional conventional loan later,” she said.Join us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

Oakley’s billionaire founder is the latest victim of the sluggish luxury housing market—but the profit he could still make shows an underlying problem

James Jannard, the billionaire founder of Oakley, has re-listed his Beverly Hills megamansion for $65 million, down from the original $68 million price listing from June 2024. Despite the price drop, Jannard stands to make a significant profit since he purchased the property for $19.9 million in 2009. This trend of wealthy sellers, including Jannard, dropping prices highlights a broader market correction where luxury buyers prioritize value and long-term security over vanity pricing.Even the wealthiest Americans are contending with today’s housing market. Take James Jannard, the billionaire founder of luxury eyewear and apparel brand Oakley, as an example. Recommended VideoJannard, who’s worth an estimated $1.3 billion according toForbes, just re-listed his Beverly Hills megamansion for an eye-popping $65 million. Still, that’s a drop from the $68 million he originally listed it for in June 2024. Oakley founder James Jannard during Launch of Oakley Thump Digital Audio Eyewear at Oakley Headquarters in Foothill Ranch, Calif. in 2004.Getty Images—Lee Celano/WireImage for OakleyHe’s fallen victim to a challenging trend in the luxury housing market where many of the country’s most lavish and expensive homes are being priced too high when they hit the market. And now, Jannard stands to lose out on the proceeds he was expecting when he first listed the house.For what it’s worth, Jannard paid $19.9 million for the property in December 2009, so even if he manages to find a buyer at the $65 million asking price, he’ll make a pretty penny for the sprawling five-bed, nine-bath concrete megamansion that stretches more than 18,000 square feet and nearly two acres in one of the most sought-after neighborhoods in Los Angeles. Orange County-based luxury real-estate firm The Altman Brothers represented the listing last year.The current listing agent on the property is Aaron Kirman with Christie’s International Real Estate, who has several listings of more than $100 million in the Los Angeles area. Kirman and Jannard didn’t immediately respond toFortune’s requests for comment about the property.Other ultra-rich home sellers have recently been forced to drop their listing prices. In May, Jennifer Lopez and Ben Affleck dropped the price of their $60 million Beverly Hills mansion by $8 million, and last year, billionaire media mogul Rupert Murdoch slashed the price of his Manhattan penthouse by nearly 40% to $38.5 million.The housing market factors affecting sellersWhile we’re not fully out of a seller’s market, the tides have begun turning in favor of buyers as listings stay on the market longer and price cuts become more common, according to Realtor.com.For that reason, price drops aren’t surprising, especially in the saturated Los Angeles luxury market where buyers have more leverage, Anthony Luna, CEO of LA-based real-estate advisory Coastline Equity, toldFortune.“Square footage and celebrity status don’t justify inflated pricing anymore,” he said. “Buyers want smart design, upgraded systems, and long-term value.”The mansion tax in LA, which applies an additional 4% tax to property sales of at least $5 million and a 5.5% tax for properties north of $10 million, further complicates real-estate sales and pricing. The cost of the tax, which is typically paid by the seller, is separate from a home’s sale price and can be a “massive amount of money,”Selling Sunsetstar and Oppenheim Group agent Emma Hernan previously toldFortune. She also described it as a “nightmare” for sellers and agents alike. Hernan said she warns her clients about the mansion tax before they prepare to sell. Take a $5 million home, for example. The seller would have to pay an extra $200,000 they “didn’t really factor in when they bought the home because the mansion tax wasn’t in play,” Hernan said.The trend of luxury-home price drops like that of Jannard, Murdoch, and Lopez say something bigger about the housing market: a larger correction, Luna said. “The luxury market is no longer about vanity. It’s about value and security,” he said. “Buyers are doing the math, and they’re calling the bluff.”Join us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

The August home sales mystery: Top analyst says ‘implausible’ housing market data ‘defies credulity’

The U.S. housing market has delivered plenty of surprises in recent years, but few as puzzling as the data released for August. According to new government figures, new-home sales surged to an annualized 800,000 units last month, up sharply from July’s upwardly revised 664,000 and far above the consensus forecast of 650,000. For a sector weighed down by rising mortgage rates, stretched affordability, and a cooling labor market, the number was so startling that one leading analyst called it “implausible.”Recommended VideoOliver Allen, senior U.S. economist at Pantheon Macroeconomics, isn’t buying it. In a research note titled US New Home Sales: Outlook grim, despite August’s implausible leap in sales, Allen says the data “defies credulity” when set against the broader trends shaping housing. He further questioned whether the headline spike accurately reflects underlying demand, or is destined to be revised away in the coming months. Calculating it as a 20.5% jump, Allen said it’s “inexplicable” that new-home sales would jump to their highest level in more than three years all of a sudden.When reached for comment, Allen toldFortunethat while discussions about the quality of U.S. economic data have “obviously been more prominent than usual this year,” given President Trump’s firing of the chief of the Bureau of Labor Statistics, he doesn’t see the implausible August data fitting into a larger pattern. “Generally speaking, the economic data in the U.S. is very comprehensive, high quality, and the statistical agencies are very clear and open about their methods.” Still, he said the new home sales numbers are a U.S. data series “well towards the lower end of the quality spectrum,” commonly featuring huge margins of error, significant revisions, and high volatility. He said the the picture for new home sales from the National Association of Home Builders (NAHB) is usually a “far more reasonable-looking description of the likely trend.”The NAHB, in fact, largely agreed with Allen in its response to the August data, albeit more restrained. Chairman Buddy Hughes, also a home builder and developer from Lexington, N.C., called it “a significant surge” and said it “may be subject to downward revision.” Still the association expects a general improvement in sales over the coming months, supported by mortgage rates declining somewhat. New-home sales have been buoyed by incentives from homebuilders, the NAHB said, citing recent survey data showing 37% of builders cut prices in August and 66% used some kind of sales incentive.Headwinds still mountingBeneath the data surprise, the structural forces bearing down on the housing market remain clear. Higher mortgage rates, tighter credit availability, and growing signs of labor-market weakness have narrowed the pool of eligible buyers. At the same time, the supply of existing homes on the market continues to recover after years of scarcity, intensifying competition for homebuilders already under pressure to move inventories.The stock of unsold new homes remains historically elevated, hitting its highest point since 2016 as of June, per the Bank of America Institute. New-home supply had surged by that point to 9.8 months—its highest point since 2022. ResiClub co-founder Lance Lambert, who closely follows data releases from public homebuilders and collects his own proprietary housing data, told Fortune in July that rising inventory means homebuyers were gaining leverage.The government report also showed a sharp monthly spike in the median sales price of a new single-family home. But Allen cautions against reading too much into that, noting the series is not seasonally adjusted and is prone to volatility. On a seasonally adjusted three-month basis, median prices continue to trend lower, suggesting discounting pressure is already emerging.Look at the larger trendMost economists now expect August sales to be revised significantly lower. Pantheon Macroeconomics projects the data will track back toward the 650,000 range in coming months—possibly falling below that threshold—as supply and affordability challenges reassert themselves.When reached for comment, Lambert toldFortunehe largely agreed with Allen regarding the August data, saying the data “seems to be suspect,” citing what public homebuilders are reporting and the data that ResiClub is collecting itself. “Most of the monthly Census homebuilder reports have a margin of error around 10% to 20%,” Lambert said. “Often really big one-month swings in that data end up being data noise. The best way to read this data is to take each individual monthly report with a grain of salt and zoom out and observe the trend.”And what trend is that? Lambert says to pay attention to the Sun Belt, which he called “the epicenter of U.S. homebuilding.” Agreeing with the NAHB survey, Lambert said softening in the Sun Belt over the past year has caused many homebuilders to offer bigger incentives and even outright price cuts to prevent a steeper pullback in new-home sales. “New-home sales have been moving sideways this year; however, if you peel back the onion, things are much choppier than headline new home sales data suggests.”[This report has been updated with additional comments from Oliver Allen of Pantheon Macroeconomics and to remove the implication that Lance Lambert saw any potential increase in activity as a result of homebuyers gaining leverage in July.]Join us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

America’s landlords settle claim they used rent-setting algorithms to gouge consumers nationwide for $141 million

Real estate giant Greystar and 25 other property management companies have agreed to collectively pay more than $141 million to settle a class action lawsuit accusing landlords of driving up housing costs by using rent-setting algorithms offered by the software company RealPage.Recommended VideoGreystar, the nation’s largest landlord, would pay $50 million under the proposed settlement agreement, which was filed Wednesday in a Tennessee federal court. The deal would still require a judge’s approval.The companies have also agreed to no longer share nonpublic information with RealPage for its rent algorithm — a key stipulation, since plaintiffs say RealPage used that information to enable landlords to align their prices and push up rents.“This represents a fundamental shift in the multifamily housing industry and will help reverse the type of anticompetitive coordination alleged in the Complaint,” attorneys wrote in the settlement filing.All companies involved in the settlement deny wrongdoing and have agreed to help plaintiffs in the ongoing case against RealPage and more than a dozen other property management firms that have not reached settlements. RealPage and others are also fighting an antitrust lawsuit filed last year by the Department of Justice and several state attorneys general. Greystar reached a settlement in that case in August.The settlement funds from the class action lawsuit would be distributed among millions of tenants included in the settlement class.In a statement, Greystar said these settlements “allow us to move forward and remain focused on serving our residents and clients.” Headquartered in South Carolina, Greystar manages more than 946,000 units nationwide, according to the National Multifamily Housing Council.RealPage has vehemently denied any wrongdoing and argues that the plaintiffs misunderstand how their product works. RealPage, which is based in Texas, has said its software is used on fewer than 10% of rental units in the U.S., and that its price recommendations are used less than half the time.“While the proposed settlements … do not include RealPage, we are encouraged to see this matter move toward closure,” Jennifer Bowcock, RealPage’s senior vice president for communications, said in a statement. “RealPage continues to believe that this litigation is without merit and that our revenue management products, and our customers’ use of them, have always been legal.”RealPage software provides daily recommendations to help landlords and their employees price their available apartments. The landlords do not have to follow the suggestions, but critics argue that because the software has access to a vast trove of confidential data, it helps RealPage’s clients charge the highest possible rent.RealPage argues that the real driver of high rents is a lack of housing supply. It also says that its pricing recommendations often encourage landlords to drop rents since landlords are incentivized to maximize revenue and maintain high occupancy.Among the other defendants, Iowa-based BH Management would pay $15 million, while Denver-based Simpson Property Group would pay $6.5 million. The other companies’ settlements range between $550,000 and $6 million.Join us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

Paris Hilton took out a mortgage on the $63 million mansion she bought from Mark Wahlberg. Here’s why that’s actually a smart financial decision

Despite Paris Hilton’s high net worth,she and her husband reportedly took out a $43.75 million mortgage for their $63 million Beverly Hills mansion, a move more common among ultrawealthy individuals than one may think. Experts say wealthy buyers often keep their cash liquid and use mortgages as a strategic tool to maximize flexibility and invest in higher-yield opportunities.Considering Paris Hilton is worth an estimated $300 million to $400 million, it might seem odd that she reportedly took out a mortgage on her recent home purchase. Recommended VideoHilton, whose vast wealth comes from 19 product lines, real estate, media and entertainment, brand partnerships, and her reality show,The Simple Life,recently bought actor Mark Wahlberg’s former estate in Beverly Hills for a whopping $63 million. But what wasn’t reported at the time was that Hilton and her entrepreneur husband, Carter Reum, reportedly took out a mortgage on the home, which might seem like an unusual move for the 44-year-old hotel heiress. And what’s seemingly even more strange is they reportedly took out the loan after they had already bought the 12-bed, 20-bath home, which shows a $43.75 million mortgage with JPMorgan Chase at an interest rate of 5.25%.But this type of arrangement isn’t as rare as it may seem, real-estate experts say. “It surprises many people, but it’s actually quite common for the mega-wealthy to take out mortgages—even when they could write a check for the full purchase price,” Evan Harlow, real estate agent at Maui Elite Property, toldFortune. In fact, public records show ultrawealthy celebrities including Beyoncé, Jay-Z, Elon Musk, and even Mark Zuckerberg have financed their homes. “The takeaway for the average buyer isn’t to mimic their precise approach, but to understand the principle,” Harlow said. “Sometimes the smartest financial move isn’t paying everything off, but keeping your money flexible and working for you.”Why the ultrawealthy take out mortgagesWhile it may seem counterintuitive to take out a mortgage in today’s market, where rates are still hovering in the 6% range, it can actually be a savvy move for ultrahigh-net-worth individuals. In fact, just because someone has the net worth to buy a home outright, that “doesn’t mean that’s how they want to allocate their cash,” Miltiadis Kastanis, director of luxury sales for Compass, based in South Florida, toldFortune.“Ultrahigh-net-worth individuals think differently about liquidity and leverage; they’d rather keep their money working for them in investments, businesses, or even art, rather than tying it all up in one property,” said Kastanis, who has represented high-profile celebrities in real estate transactions.In other words, using a mortgage helps to free up capital for higher-yield investments or business ventures, according to Harlow. He used the example of one of his clients, the owner of a successful tech business, who recently purchased a $3 million property and decided on a jumbo loan. The client didn’t have to do that, but he wanted to keep his cash in the market, where his portfolio, over the long term, was reaping annualized returns well over the mortgage rate. “For him, buying a house with cash sounded like ‘just parking money in the driveway,’ as opposed to putting it to work,” Harlow said.Both Harlow and Kastanis also said ultrahigh-net-worth individuals see mortgages differently from other people. People like Hilton view it more as a tool instead of a burden. “For many wealthy buyers, a mortgage is just another lever they can pull in their overall wealth strategy,” Kastanis said. “They’re playing chess, not checkers.”Join us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

A gauge of future home sales just turned negative—despite 9 straight weeks of falling mortgage rates

Mortgage rates have been coming down, but there has yet to be a spike in homebuying activity—and one leading indicator has even declined.Recommended VideoPending home sales, or signed contracts leading up to a sale, fell for the first time in nearly three months, slipping about 1% during the four weeks ending Sept. 21 compared to a year earlier, according to a Redfin report on Thursday.That’s despite the weekly average mortgage rate sliding for nine consecutive weeks, hitting an 11-month low of 6.26% after reaching 6.8% at the start of the summer.Meanwhile, separate data from the National Association of Realtors on Thursday showed that sales of existing homes dipped 0.2% in August from the prior month. While they were up 1.8% from a year ago, the recent trend still points to a stagnant housing market.To be sure, lower mortgage rates have sparked a surge in at least one corner of the housing market. Redfin pointed out that mortgage applications to refinancehomes jumped 58% in the second week of September from the prior week.But mortgage-purchase applications edged up just 3%, and the anemic sales data are dashing hopes that cheaper borrowing costs will quickly jump start the housing market.Redfin highlighted four factors weighing on housing demand: still-elevated home prices, would-be buyers waiting for mortgage rates to go below 6%, muted supply of new listings, and economic uncertainty.Those waiting for mortgage rates to fall further may have already missed their chance, as borrowing costs have started to tick higher again.According to Mortgage News Daily, top-tier 30-year fixed rates were in the high 6.3% range on Friday, flat from the previous Friday but up from 6.1% range in the first half of last week.That’s as recent economic data have come in hot, lowering expectations for aggressive rate cuts from the Federal Reserve. As a result, Treasury yields have rebounded, lifting borrowing costs elsewhere, including mortgage rates.Meanwhile, job growth hasn’t been as robust as other indicators have been, casting gloom over the housing market. In addition, uncertainty about President Donald Trump’s tariffs and recession fears still linger, according to Redfin.“A lot of buyers are hesitating because they’re worried about potentially losing their jobs, losing money in their stock portfolio, and the economy in general,” said Josh Felder, a Redfin Premier agent in San Francisco, in a statement. “Many of the buyers who are moving forward are making offers with contingencies, and are willing to walk away during the inspection period if they don’t get the concessions they want.”Join us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

Florida’s housing market was skewed wildly by the pandemic. It’s finally coming to grips with a ‘realistic middle ground’

The housing market in Florida is in the midst of a major change: Inventory is down for the first time in 110 weeks, according to Compass chief economist Mike Simonsen. But it’s not for the reason you might think.Recommended VideoFlorida’s housing market was one of the hottest during the pandemic due to the state’s appeal to remote workers, retirees, and investors who relocated from high-cost states like New York and California seeking more space, lower taxes, and lenient COVID restrictions. Between March 2020 and June 2022, prices rose a whopping 51%. Demand was high, so inventory was low. But now, Florida’s inventory levels are dwindling for a very different reason. Experts say that it’s not revived demand, but rampant delistings and fewer new listings that are causing the change. Home prices are down about 5.4% year over year, according to Zillowdata. “Low prices and low demand are making people who aren’t in a hurry simply withdraw listings rather than sell at a low price,” Alexei Morgado, a Florida real estate agent and founder of real-estate exam prep company Lexawise, toldFortune. “Inventory is down, but not because of big sales, but rather because of [delistings] and slow demand. So it’s all a mixed bag.”Realtor.com data for August show some parts of Florida saw nearly 60 homes delisted for every 100 newly listed homes. Miami had the highest delisting-to-listing ratio with about 59, while Tampa had 33 and Orlando had 28.Overall, the number of single-family homes for sale in Florida fell from more than 100,000 in the spring to about 96,000, after years of rapid growth, according to Simonsen, who is also the founder and president of real-estate analytics firm Altos Research. This downward trend is a signal the market is “clearing out” the would-be sellers, Jenna Stauffer, a Florida-based real-estate broker and global real estate advisor for Sotheby’s International Realty, toldFortune.The ones who needed to sell have most likely already done so, even if it meant lowering prices or offering concessions. Stauffer said the pullback is “healthy,” though, because it helps reset home prices and balances out supply and demand. “It also shows that sellers are becoming more in tune with market conditions,” she said. Is the Florida housing market crashing or correcting?While experts say Florida’s housing market is experiencing some major changes, they aren’t indicative of a crash—which would be a swift and severe decline in prices driven by an imbalance of supply and demand.Rather, experts say the trend of inventory declines is a sign the Florida housing market is correcting itself. “Higher inventory had been putting downward pressure on prices and giving buyers the upper hand,” Stauffer said. “Buyers had so many options, no urgency and plenty of time to negotiate.”But now that inventory is tightening, the dynamic could start to shift, she said, because buyers will lose a little bit of that leverage they had and sellers could regain “a little” power. Stauffer also said it’s “not a crash in Florida, but a reset.” Sellers “have to recognize that this is a different market than a few years ago,” she added. “Demand isn’t the same and supply isn’t the same. It’s forcing everyone to a more realistic middle ground.”And for that reason, it may not be the best time to sell your home in Florida, Morgado said—but it could be the right time to make a purchase.“You can sell if necessary, of course, but wait if you can,” he said. “And for buying: You can get [a] good price, with lower rates and discounts, so take advantage of [that] now.”Join us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

Housing costs are so high some Americans are delaying milestones like getting married, having kids and even adopting a pet

Americans are sacrificing a lot just to be able to afford a roof over their head. Recommended VideoAccording to a recent Redfin survey, more than 44% of U.S. homeowners and renters said they struggle to afford their mortgage or rent payments. And because of that, they’ve been forced to forgo dining out at restaurants and taking vacations. But what’s more alarming is they’re delaying major life milestones like getting married and having children. That’s according to a Redfin-commissioned survey conducted by Ipsos in May of more than 4,000 U.S. homeowners and renters. That curtails with previous reporting fromFortuneshowing how high housing costs and other life expenses have forced Gen Z and millennials to delay the American Dream.“We’re shining a light on [these homeowners and renters] because they speak to the lengths people go to make their housing payments,” according to Redfin.Even though having pets became somewhat of the new craze for Gen Z and millennials who knew they couldn’t afford to have human children, that’s seemingly become too expensive on top of housing costs. Some people even report staying in a marriage or relationship longer than they wanted because they couldn’t afford housing plus a divorce or to live on their own.The following are sacrifices Americans have made in order to afford housing, according to the Redfin report:Moved in with parentsMoved in with other family membersMoved in with roommatesMoved in with a romantic partnerI had to give up my pet(s)Gave up or reduced college savings for their kidsDecided against or delayed having a childEnrolled my child(ren) in a low-rated schoolMoved in with my grown childrenPostponed getting a divorce or separationAnd it shows in more data: The housing market has become so unaffordable for Gen Z and millennials, the number of first-time home buyers shrank to a historic low. The number of first-time homebuyers in 2004 was nearly 3.2 million, according to NAR data shared withFortunein July Tuesday. By late 2024, that number had plummeted to just 1.14 million.“We’re seeing a reshaping of the housing ladder,” Alexandra Gupta, a real estate broker with The Corcoran Group, previously toldFortune. The firm was founded by Shark Tank star, investor, and real estate legend Barbara Corcoran. “Some first-time buyers are turning to long-term renting or even co-living models because the idea of owning a home has become so out of reach,” Gupta added, while others are relying on family support.Meanwhile, Americans continue to struggle with housing payments because the pace of wage growth doesn’t match the clip at which home prices are growing. Home prices in the U.S. are more than 50% higher than they were right before the pandemic, but incomes haven’t increased enough.To combat that challenge, many younger buyers are considering buying (or continuing to rent) with friends or family.“Young buyers are adapting out of necessity and out of determination. They’re willing to do whatever it takes to build equity and stability, even if that means approaching ownership in ways their parents never considered,” Niles Lichtenstein, cofounder and CEO of real-estate platform Nestment, toldFortune. “Co-buying is a reflection of both the constraints of the market and the ingenuity of this generation.”Join us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

Now is the worst time to flip a home. It hasn’t been this bad in nearly two decades

It pays less and less to buy and flip a home these days. From April through June, the typical home flipped by an investor resulted in a 25.1% return on investment, before expenses. That’s the lowest profit margin for such transactions since 2008, according to an analysis by Attom, a real estate data company.Recommended VideoGross profits — the difference between what an investor paid for a property and what it sold for — fell 13.6% in the second quarter from a year earlier to $65,300, the firm said. Attom’s analysis defines a flipped home as a property that sells within 12 months of the last time it sold.Home flippers buy a home, typically with cash, then pay for any repairs or upgrades needed to spruce up the property before putting it back on the market.The shrinking profitability for home flipping is largely due to home prices, which continue to climb nationally, albeit at a slower pace, driving up acquisition costs for investors.“We’re seeing very low profit margins from home flipping because of the historically high cost of homes,” said Rob Barber, Attom’s CEO. “The initial buy-in for properties that are ideal for flipping, often lower priced homes that may need some work, keeps going up.”The median price of a home flipped in the second quarter was bought by an investor for $259,700, a record high according to data going back to 2000, according to Attom.The median sales price of flipped homes was $325,000, unchanged from the first quarter, the firm said.A chronic shortage of homes on the market and heightened competition for lower-priced properties are also helping drive up investors’ acquisition costs.Home flipping profits have declined for more than a decade as home prices rose along with the housing market’s recovery from the housing crash in the late 2000s.Consider, in the fall of 2012, the typical flipped home netted a 62.9% return on investment before expenses, Attom said.Even as home flipping has become less profitable, such transactions remain widespread.Some 78,621 single-family homes and condos were flipped in the April-June quarter, accounting for 7.4% of all home sales during the quarter — a slight decline from both the first quarter and the second quarter of 2024, according to Attom.The U.S. housing market has been in a sales slump since early 2022, when mortgage rates began to climb from pandemic-era lows. Sales of previously occupied U.S. homes sank last year to their lowest level in nearly 30 years. Sales have remained sluggish this year as mortgage rates, until recently, remained elevated.As home sales have slowed, properties are taking longer to sell. That’s led to a sharply higher inventory of homes on the market, benefiting investors and other home shoppers who can afford to bypass current mortgage rates by paying in cash or tapping home equity gains.With many aspiring homeowners priced out of the market, real estate investors — whether those looking to buy and rent or home flippers — are taking up a bigger share of U.S. home sales overall.Some 33% of all homes sold in the second quarter were bought by investors — the highest share in at least five years, according to a report by real estate data provider BatchData.Between 2020 and 2023, the share of homes bought by investors averaged 18.5%.All told, investors bought 345,752 homes in the April-June quarter, an increase of 15% from the first quarter, but a 12% decline from the same period last year, the firm said.Even so, investor-owned homes account for roughly 20% of the nation’s 86 million single-family homes, the firm said.Join us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

The U.S. housing market is in spooky season: 15% of home sellers are getting ghosted by buyers

Halloween is just about a week away, but spooky season started early for the U.S. housing market. Recommended VideoIn September, more than 53,000 home-purchase agreements were canceled—or 15% of all homes under contract, according to Redfin data released Wednesday. That’s nearly a 14% jump from the same time last year. The housing markets with the highest percentage of pending sales that fell out of contract include: Minneapolis (11%)Boston (10%)New York City (9.6%)Seattle (9.5%)Montgomery County, Pa. (9.2%)Buyers are ghosting sellers because—considering high home prices and mortgage rates—they expect homes to be near-perfect to follow through on a contract, according to Redfin. Plus, Jo Chavez, a Redfin Premier agent in Kansas City, Mo., said in a statement he’s seeing “a lot of buyer’s remorse.”“Buyers make an offer, then they start worrying they could have found a better deal or a better home because there are more home sellers than buyers in the market,” Chavez said. “Some other buyers are backing out because they’re concerned about job security.”Americans are so worried about the economy, in fact, a recent Fannie Mae survey showed a whopping 73% of them said it’s a bad time to buy a house. Meanwhile, only 32% of consumers said they expect their personal finances to improve during the next year, and 23% said they think things will get worse. But aside from overall economic anxiety, buyers and sellers are failing to agree on concessions and repairs, according to Redfin. That’s a major shift from the pandemic-era housing market in which many buyers chose to forgo concessions and repairs in hopes of presenting a more favorable offer in a highly competitive housing market. That dynamic has flipped though, with the housing market showing signs its turning in favor of buyers. “For prospective buyers who have been waiting on the sidelines, the housing market is finally starting to listen,” wrote chief economist Mark Fleming in an Aug. 29 First American post. That’s due to home price growth that is mostly flat or slightly declining because of decreasing demand and increasing supply, according to the National Association of Home Builders. Redfin also says it’s a buyer’s market in most of the U.S.—and that’s why so many transaction cancellations are happening. “Those who are still in the market know they have leverage,” according to Redfin. “It’s common to be choosier and ask for repairs, price reductions and other concessions. When sellers push back, or when inspections reveal new issues, many buyers are walking away.” Climate risks in the Sunbelt region have also discouraged some buyers from following through on contracts, according to Redfin. Some sellers are delisting homesWhile many buyers are pulling out of home purchase agreements, some sellers are also pulling their homes off the market. “It’s a clear signal that buyers are holding more of the power right now, especially with inventory climbing and [mortgage] rates staying elevated,” Anthony Djon, founder of Anthony Djon Luxury Real Estate in Detroit, previously toldFortune. That’s because they’re not getting the offers they think they deserve for their homes, and average time on the market is increasing. A recent Realtor.com report shows the typical home has spent 62 days on the market, a week longer than the same time last year. “What we’re seeing nationally is a market that’s gradually rebalancing, with buyers gaining leverage and sellers facing a tradeoff: Adjust to the market and sell for less, or hold out and risk sitting indefinitely,” Realtor.com Senior Economist Jake Krimmel previously toldFortune. “Many sellers still aren’t pricing to sell.”Redfin suggests that to keep home purchase agreements in place, sellers should get a pre-inspection, be realistic and flexible with concessions and repairs, and price the home appropriately. Even though buyers are “in the driver’s seat in much of the U.S.,” according to Redfin, they should still plan to get pre-approved, research insurance costs and HOA fees, and back out only if there are major issues or repairs needed that are unreasonable.Join us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

Cape Cod is considering taxing luxury home sales of $2+ million to raise funds for the housing market’s ‘missing middle’

Cape Cod, one of the priciest housing markets in the U.S., is considering a 2% real-estate transfer fee on luxury homes above $2 million to fund affordable housing. Similar “mansion taxes” in Los Angeles and Rhode Island show how other expensive markets are turning to surcharges on wealthy homeowners to redistribute housing wealth.Cape Cod is one of the most expensive housing markets in the U.S. While the median home price in the beachy region of Massachusetts is about $600,000, waterfront properties and homes in exclusive areas often exceed $1 million, according to Warren Buffett’s Berkshire Hathaway Home Services.Recommended VideoAnd luxury homes in the region might get even more costly as Cape Cod lawmakers consider a tax on wealthy homeowners. The proposal, currently before the Barnstable County Assembly of Delegates, would tack on an extra 2% surcharge on luxury-home sales above $2 million.The goal of the proposed real-estate transfer fee is to generate up to $56 million per year for affordable and year-round housing to make Cape Cod a place where “working families, seniors, and young people can afford to live,” according to the Falmouth Democratic Town Committee.Since housing is so expensive on the Cape, the majority of homeowners there include affluent second-home buyers, pre-retirement couples, high-paid remote and hybrid workers, and investors, according to Massachusetts-based real-estate firm Guthrie Shofield Group. “We’ve always been a place where the wealthy or affluent come to vacation and when they come to vacation, it’s typically service-based employees and that workforce waiting on them,” Alisa Magnotta, CEO of Hyannis, Mass.-based Housing Assistance, said in a statement.Indeed, homeowners for a majority of the towns on Cape Cod need to make about $200,000 to $300,000 or more per year to afford to buy a home there, according to Housing Assistance. Meanwhile, Cape Cod workers’ wages are much lower when compared to the rest of the state: While the median household income in Massachusetts is about $101,000, according to Housing Assistance, the median income in many Cape towns is just about $70,000 to $80,000.“A transfer fee is not a tax on regular people—it’s a way to reallocate some of the wealth from second or third home buyers to support the people who make this community what it is,” Ella Sampou, a community organizer with the Lower Cape Community Development Partnership, said in a statement.Therefore, the property exchange fee could help build for the “missing middle,” or a range of housing options like duplexes, townhomes, or apartment complexes that are often more affordable than single-family homes for the average wage earner.Other expensive cities with extra real-estate taxesCape Cod isn’t the first expensive housing market to introduce an extra real-estate tax on the wealthy. Similarly, the so-called “mansion tax” in Los Angeles tacks on an additional 4% tax to property sales of at least $5 million and a 5.5% tax for $10 million-plus properties. The cost of the tax is typically paid by the seller, and is something separate from a home’s sales price, but can be a “massive amount of money,”Selling Sunsetstar and Oppenheim Group agent Emma Hernan previously toldFortune. On the flipside of the argument about a real-estate tax on luxury properties, Hernan also described it as a “nightmare” for both sellers and agents. In LA, for example, someone selling a $5 million home would have to pay an extra $200,000 they “didn’t really factor in when they bought the home because the mansion tax wasn’t in play,” Hernan said.There’s also a mansion tax in Rhode Island targeting luxury second homes and non-owner-occupied properties. It’s commonly referred to as the “Taylor Swift Tax” since the pop star owns a $17 million mansion there. Beginning next year, Rhode Island will slap a surcharge on vacation homes in the state that are worth at least $1 million. Mansion owners will have to pay $2.50 for every $500 of assessed value above the first million. For Swift, that would be an extra $136,000 in property taxes. (A Cape Cod home previously owned by Swift just recently went up for sale for $14.5 million). Join us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

AI startups are leasing luxury apartments in San Francisco for staff and offering large rent stipends to attract talent

The AI boom is bringing a wave of startups to San Francisco, and employees are receiving generous benefits in one of the country’s priciest housing markets. Recommended VideoRoy Lee, CEO of AI tech startup Cluely, which makes software for job interviews and work calls, toldThe New York Timesthat he leased eight apartments for employees in a recently-built luxury complex situated just a one-minute walk away from the office. The rents in the 16-story building range from $3,000 to $12,000 a month. “Going to the office should feel like you’re walking to your living room, so we really, really want people close,” Lee toldThe Timeson Thursday.Flo Crivello, CEO of Lindy, another AI startup, said he offers his approximately 40 employees a $1,000 rent stipend every month if they live within a 10-minute walk of the company’s office.“People are so much happier and healthier when they live close to work,” he toldThe Times. “This makes them stick around for longer, perform better and work longer hours.”The AI boom has drawn a flood of money and talent to San Francisco, inflating rent in the process. The Bay Area has attracted 70% of AI venture capital funding nationwide since 2019, according to data from Pitchbook. Across the U.S. and Canada, the pool of tech workers with AI skills jumped more than 50% to 517,000 from mid-2024 to mid-2025, according to a September CBRE report. The San Francisco Bay Area, New York metro and Seattle are the top U.S. markets for AI-specialty talent, accounting for 35% of the national total, the report said.Meanwhile, fully remote working arrangements for open positions have declined, and more employers are adopting hybrid arrangements requiring tech talent to spend three or more days in the office. In San Francisco alone, 1 out of every 4 square feet of office space was leased by an AI company over the last two and a half years, according to CBRE.Tightness in the office market is also seen in the residential sector. Over the past year, apartment prices in San Francisco rose 6%, on average, more than twice the 2.5% increase experienced in New York City and the highest rate in the nation, according to real estate tracker CoStar data cited byThe Times. In hot spots like Mission Bay, near OpenAI’s headquarters, rents climbed 13% recently.Average rent for a San Francisco apartment is now $3,315 a month, just below New York City’s, the nation’s highest at $3,360.A September report from real estate tech company Zumper said San Francisco’s housing market bucked the national trend of flat or falling prices and instead saw the strongest annual growth across the country for two-bedroom rent, which surged 17.1%. One-bedroom rent climbed 10.7%, the third-highest increase in the nation, the report said.The report points to a “perfect storm” of tech-sector hiring and stricter return-to-office mandates driving more renters into the city as well as supply-chain constraints. The city’s vacancy rate has fallen back to pre-pandemic levels, and new housing construction is at its weakest pace in a decade, the report added.Will Goodman, a principal at Strada Investment Group, which developed the luxury complex where Cluely leased its eight apartments, toldThe Timesthat half of the 501 units in the complex were leased within two months of its May opening.“Honestly, I’ve never seen anything like it before,” he saidJoin us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

The housing market is no longer a wealth-building engine as home prices continue to slump

Home prices aren’t keeping up with inflation, representing a drag on wealth in real terms, according to S&P Global. That’s as home prices have been falling on a monthly basis, while President Donald Trump’s tariffs have kept inflation sticky and still-high mortgage rates have weighed on demand.High home prices and mortgage rates have created unaffordable conditions for many Americans, but the housing market’s ability to create more wealth has sputtered.Recommended VideoThat’s because even as home prices continue to hover around record levels, they are also edging lower and lagging behind the rate of inflation, which has heated up amid President Donald Trump’s tariffs.“For the first time in years, home prices are failing to keep pace with broader inflation,” said Nicholas Godec, head of Fixed Income Tradables & Commodities at S&P Dow Jones Indices, in a statement on Tuesday. The last time that happened was mid-2023.The latest S&P Cotality Case-Shiller home price data showed that the 20-city index fell 0.3% in June from the prior month, marking the fourth consecutive monthly decline.On an annual basis, the 20-city composite was up 2.1%, down from a 2.8% increase in the previous month, and the national index saw a 1.9% yearly gain, down from 2.3%. Meanwhile, the consumer price index rose 2.7% in June from a year ago.“This reversal is historically significant: During the pandemic surge, home values were climbing at double-digit annual rates that far exceeded inflation, building substantial real wealth for homeowners,” Godec added. “Now, American housing wealth has actually declined in inflation-adjusted terms over the past year—a notable erosion that reflects the market’s new equilibrium.”Weak prices suggest underlying housing demand remains muted, he said, despite the spring and summer historically being the peak period for homebuying.In fact, this year’s selling season has been a bust. While sales of existing homes have ticked up recently, they are still subdued and prices are flat. In addition, sales of new homes are slumping with prices down.Conditions have been so dire that Moody’s Analytics chief economist Mark Zandi sounded the alarm on the housing market even louder last month.In Godec’s view, the recent shift in the housing market could represent a new normal—but one that also has a positive angle.“Looking ahead, this housing cycle’s maturation appears to be settling around inflation-parity growth rather than the wealth-building engine of recent years,” he said.That’s as pandemic-era hot spots in the Sun Belt have cooled off with demand increasingly tilting toward established industrial centers that enjoy sustainable fundamentals like employment growth, greater affordability, and favorable demographics.“While this represents a loss of the extraordinary gains homeowners enjoyed from 2020-2022, it may signal a healthier long-term trajectory where housing appreciation aligns more closely with broader economic fundamentals rather than speculative excess,” Godec added.Meanwhile, analysts at EY-Parthenon sounded gloomier about the housing market in a report that also came out on Tuesday, predicting that home prices will turn negative on an annual basis by year-end due to low demand and rising inventories.Home listings are up 25% from a year ago, and inventories have risen for 21 consecutive months. Homebuilders are also cautious given that demand is under pressure and construction costs are still elevated.“Looking forward, the housing market is expected to stay stagnant, as slowing income growth and persistently high borrowing costs continue to limit demand,” the EY report said. “While proposed changes to the regulatory environment can help improve builder sentiment, elevated construction costs due to higher tariffs along with ample inventories will continue to constrain construction activity.”Join us at the Fortune Workplace Innovation SummitMay 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

‘Oracle of Wall Street’ says boomers control the housing market, and their enormous equity will keep them in place — ‘There will be no quick fixes’